THE UPSIDE OF THE DOWNSIDE - PART IIIA

Why Another Stock Market Crash and Great Depression are Inevitable

The wonkiness deepens, and the bad news continues. This will be a long post, but it’s essential to understanding why another stock market crash and great depression are inevitable. It is divided into two parts: IIIA and IIIB. Don’t lose heart. This, too, shall pass. In future posts, I will offer suggestions on how we can cope with approaching hard times and thrive both as individuals and as a virtuous society when good times return.

A quick review and look ahead:

Part I of this series set the basic bad-news/good-news premise: 2024 is the new 1928 in terms of the surging economy, soaring financial markets, and politics. The rhymes of history suggest the aftermath of the 2024 election will include a rerun of the 1929 Crash and the Great Depression of the 1930s, prompting a backlash given the rise of the state-active Roosevelt administration. Such a shift in political sentiment would drive the liberal/progressive agenda needed to repudiate the oligarchy, rebuild the middle class, restore democracy, reform and rebalance the government, and reconstruct the economy to meet the necessities of the new technological era.

Part II reviewed the financial and economic record of the past two centuries in the U.S., dating from the end of the Agricultural Age (technically the Neolithic Revolution) to the present, revealing three completed revolutionary (and, ultimately, global) Megacycle transformations (the two Industrial Revolutions and the Computer Revolution) each unfolding in three phases: Phase I exponential economic growth and soaring stock markets; Phase II economic, financial and political trauma and war; Phase III sustained, mature postwar economic growth with normal business cycles. The current soaring stock market and continuing economic expansion (Phase I) of the fourth Megacycle, the Artificial Intelligence Revolution, ongoing for the past decade, suggests that the “good times” of its first phase may continue for a while longer. However, repetition of the earlier Megacycle patterns raises the expectation of another Phase II crash and great depression á la 1929 and 1930s. Whether the conclusion of such a Phase II includes domestic violence and war remains to be seen.

Just as Calvin Coolidge handed off a booming economy to Herbert Hoover, Joe Biden is handing off a similarly booming economy to Donald Trump. As we approach the most dangerous phase of the current Megacycle with the most dangerous president in U.S. history at the helm, what could possibly go wrong?

Part III below delves more deeply into the mechanics of the anticipated Phase II crash and great depression and reveals the structural economic and financial forces creating and triggering this trauma. Bear in mind: the repetitive nature of Megacycles reflects consistent, unchanging human nature expressed collectively in response to a global economy evolving through technological change. Humankind collectively possesses short memories and scant ability to learn from past mistakes, hence: “Those who cannot remember the past are condemned to repeat it.” (George Santayana) Individuals, however, can remember the past and, thus acquitted, thrive. I’ll show you how in future posts of this series.

WHAT MAKES A STOCK MARKET CRASH AND A GREAT DEPRESSION INEVITABLE? Income Distribution: The Mechanism Creating Turmoil in Phase II of Megacycles

Because the collective behavior demonstrated in Megacycles derives from fundamental laws of nature, let’s begin with first principles: All life depends on the successful exercise of its most fundamental instinct: survival, manifested as an irresistible impulse to live and aversion to death. In turn, the survival instinct to live depends upon “energy efficiency,” gaining as much or more “energy” through exertion than expended. This quest for life and aversion to death drives all life to seek the greatest possible reward for the least amount of energy expended. Every living organism, from a Mycoplasma bacterium to a blue whale and on up to a giant sequoia, abides by this principle until it doesn’t; then it withers and dies. This cycle of life from birth to death progresses in three phases: 1) Growth (in which the amount of energy gained exceeds energy expended), 2) Trauma, causing 3) Decline (in which energy expended exceeds energy gained), ending in death. Successful species achieve continuity by reproducing, usually in the growth phase, producing offspring capable of adapting to a changing environment through the process of evolution. Humankind is no exception to these rules of life and must, therefore, abide by that instinct, that principle, and that cycle, both individually and collectively, as enterprises and polities. Part II of this series revealed that fundamental cycle for the U.S. polity and, by extension, globally, as a Megacycle.

What has made humankind the most successful species on earth is its intellectual capacity to not only adapt to a changing environment over time but also to change its environment to its advantage in a process analogous to successful evolutionary reproduction ensuring continuity of species. Such changes occur through innovation: the development of tools (i.e. technology) increasing the production of “energy” (sustenance and other essentials and comforts of life) while reducing the exertion required to produce it. Economists call this phenomenon “gains in productivity.” Human beings and their enterprises and polities survive by producing goods and services (“energy” acquired through exertion), the value of which exceeds the costs of production (“energy expended”); the difference between the two is “profit” or “surplus.”

We humans thrive by innovating through the development of new technologies of production, creating spectacular gains in productivity manifested as economic “revolutions” (as in “Industrial Revolution”), each revolution progressing in three phases analogous to the previously described “cycle of life.” Beginning with the explosive growth of Phase I, a disproportionate share of extraordinary corporate profits and related stock appreciation derived from productivity gains accrue to the managers and owners of the new enterprises associated with the new technology, creating huge investable surpluses. However, as explained below, participation by the working classes invariably lags the lion’s share apportioned to the rich elite (variously called “Robber Barons,” “Malefactors of great wealth,” plutocrats, oligarchs, etc.). This lopsided distribution of the fruits of progress (i.e. “inequality.”) sets up the preconditions for Phase II, as described in the graphs below.

Labor’s share of the fruits of economic progress has varied considerably throughout the course of each Megacycle but, as previously stated, invariably lags the share of the gains apportioned to the rich elite.

During the First Industrial Revolution, 19th-century workers endured Dickensian “starvation wages,” as explained by Marx and Engels, largely due to the flood of farmers displaced by the mechanization of agriculture into urban factories and the concentration of economic and political power in the hands of factory owners.

During the 1920s, in Phase I of the Second Industrial Revolution, workers benefitted unequally. Those associated with the earlier Megacycles (e.g. coal, steel, and agriculture), fared poorly, resulting in occasional strikes often suppressed with violence. Those workers associated with electro-mechanical technology, such as assembly-line work at factories producing automobiles, appliances, and radios, enjoyed rising real wages and standards of living, an 8-hour workday, company benefits, and participation in the burgeoning debt-financed consumer culture fueling the “Roaring Twenties.”

Since the Computer Revolution, beginning around 1980 and coinciding with the “Reagan Revolution” (dedicated to the enrichment of the upper classes and immiseration of the rest), the rich became stupendously richer, the poor remained poor, and the middle class marked time with many joining the ranks of the poor. (See: “Distribution of Household Wealth in the U.S. since 1989”) Individually, the same disparity of reward exists between those workers associated with the new technology and those associated with older technologies who, predictably, constitute the core of the angry Right these days. Collectively, however, the working classes have not received a real pay increase (adjusting for inflation) since Reaganomics began cutting taxes for the rich, raising them for the rest, disbanding unions, underfunding education, rolling back regulations, and ginning up Department of Defense contracts. A distressing number of workers experience the Dickensian “starvation wages” of their forebears; living paycheck to paycheck; spending nearly everything they earn; not saving much, if anything; living under the threat of medical bankruptcy and homelessness (thankfully, they’ve done away with debtors’ prisons); struggling to pay down student loans, mortgages, and credit card debt bearing usurious rates of interest. At least, unlike their forbears, they can depend on Social Security to pay their basic bills in old age (although even that is questionable if die-hard Republicans get their way).

The Consequences of Income/Wealth Inequality

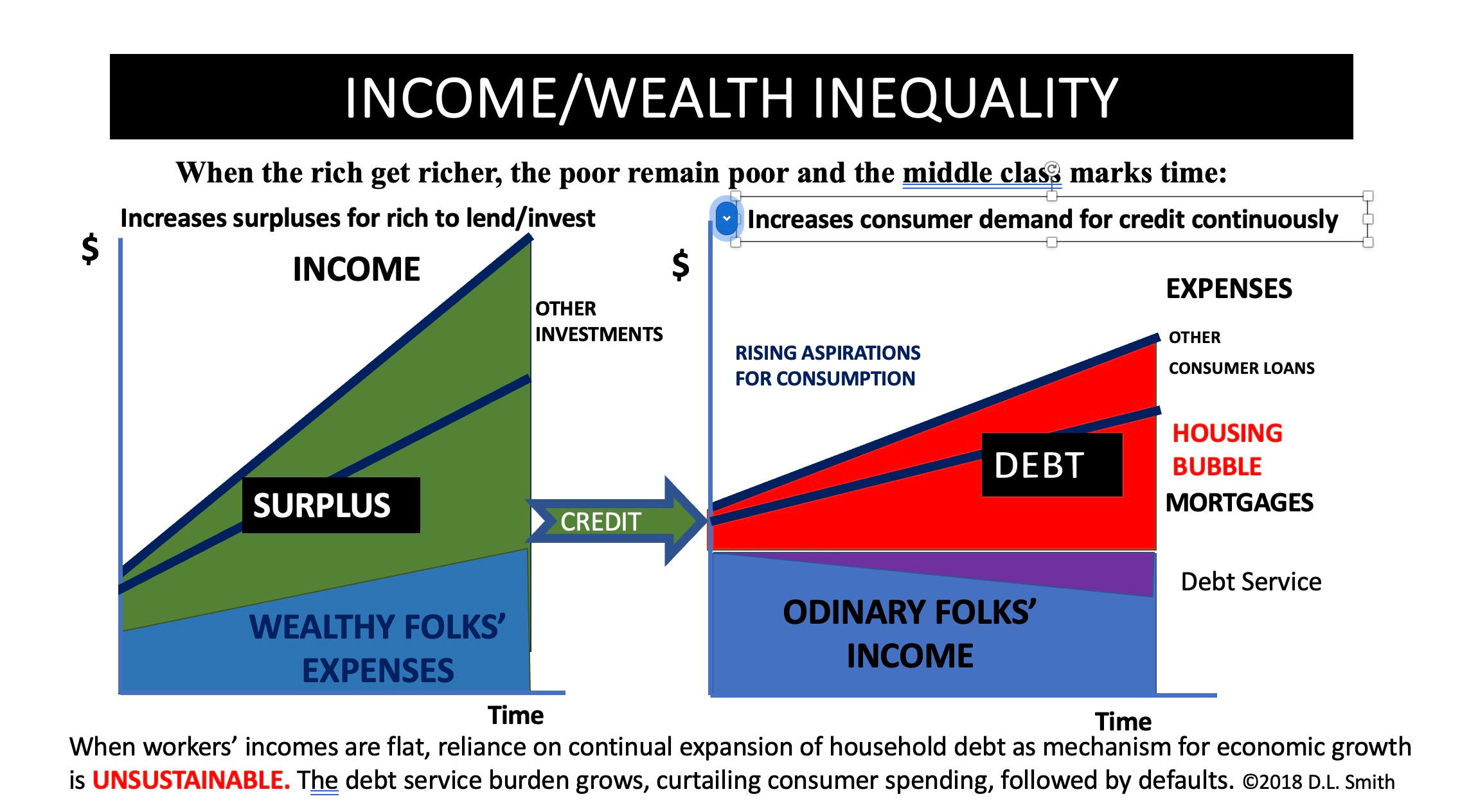

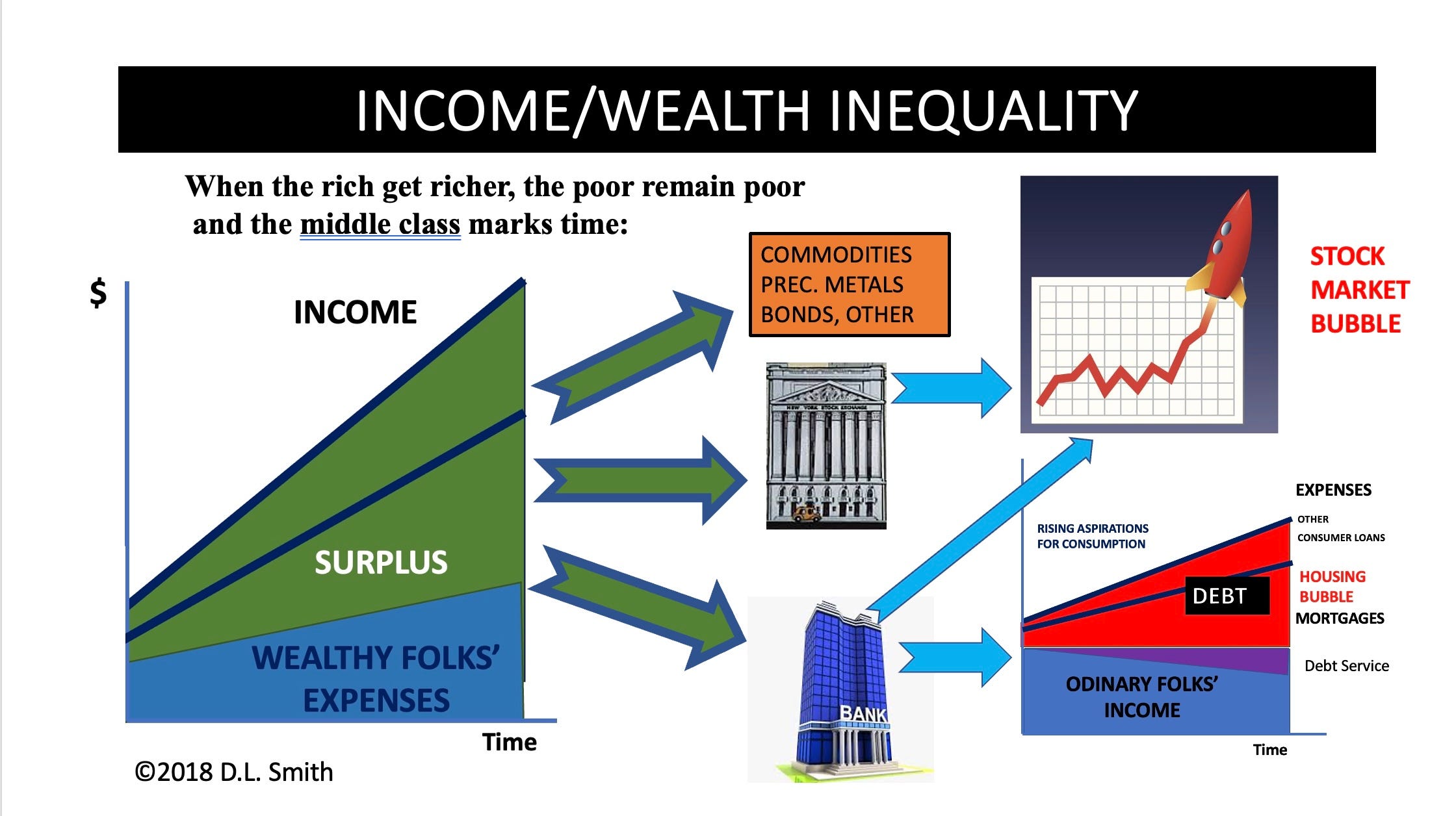

Even with extravagant spending on mansions, yachts, private jets, travel, jewelry, etc., members of the wealthy elite don’t spend everything they earn, leaving vast surpluses available to invest. Economists refer to this behavior as a lower marginal propensity to consume and a higher marginal propensity to save. Accordingly, the surpluses of the rich flow copiously into stocks and bonds and, through the intermediation of banks, into household credit and mortgages, driving real estate prices skyward while burdening the working classes with ever-increasing amounts of debt, as shown below.

The graph above shows one aspect of the flow of funds from the surpluses of the wealthy as they capture the lion’s share of economic growth, namely deposits in banks. Banks then lend about three-quarters of these deposits to homeowners as mortgages and the rest as consumer loans (credit cards, installment purchases, etc.) and to businesses (shown in the second graph below). This credit (i.e., consumer debt) fills the gap between workers’ stagnant wages and rising aspirations for consumption in fulfillment of the American Dream advertised by corporations eager to profit from satisfying these aspirations. With the passage of time, this geometry results in an ever-increasing debt burden, the associated debt service of which erodes spendable income until consumers either stop borrowing or default – either way, corporate sales and profits plunge, inducing a stock market crash, dragging the economy deeply into recession or, if particularly severe, depression.

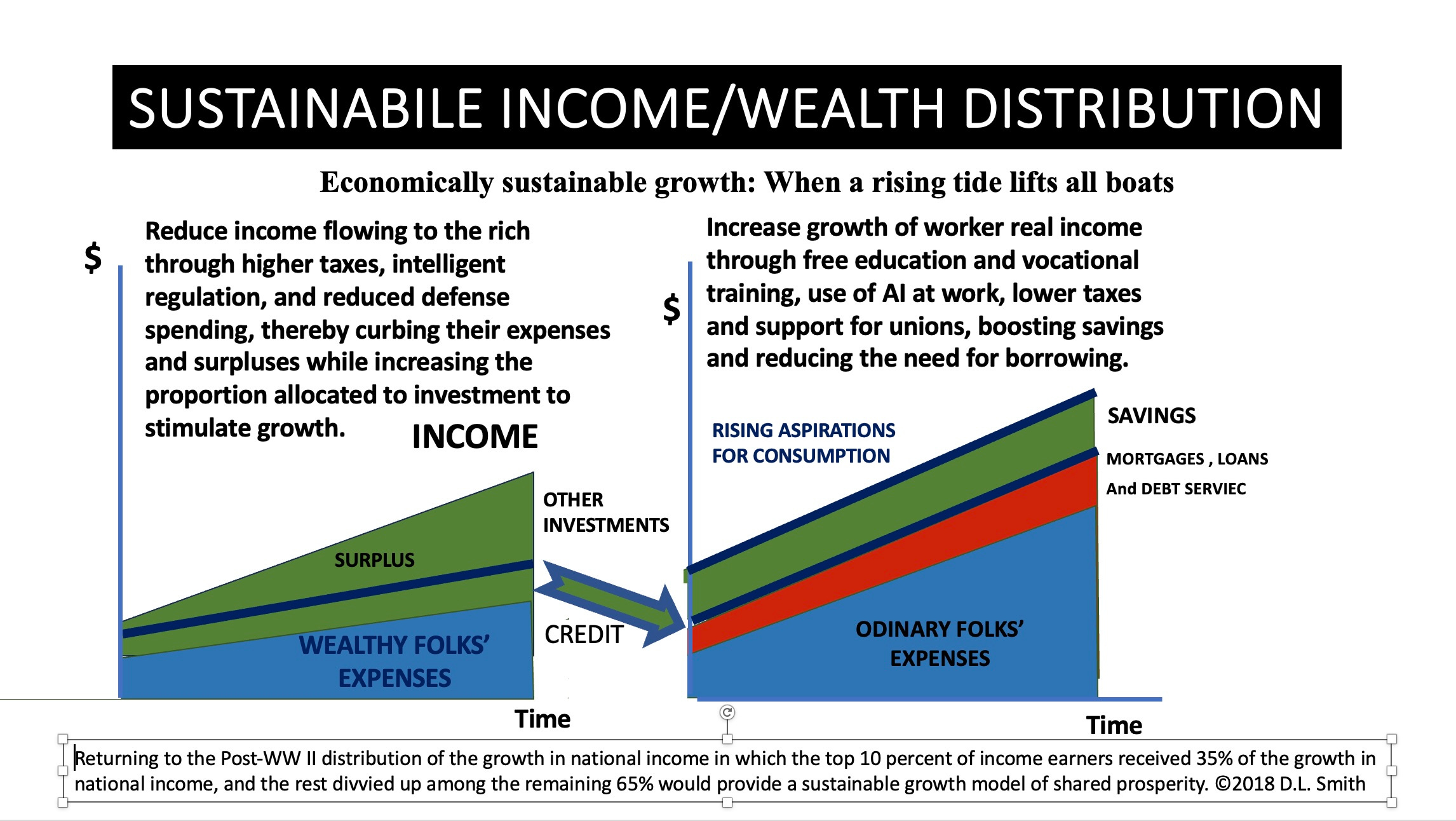

By contrast, the graph below shows a sustainable, more equitable income distribution in which a rising tide lifts all boats, not just the yachts of the wealthy elite. This model would require a lesser share of the productivity gains in Phase I to go to the managers and owners and a correspondingly larger share to go to the working classes.

Such a pattern of income distribution would produce the following results:

The extraordinary wealth generated by gains in productivity initiated in Phase I would be shared more equitably (as in the post-World War II period) between the rich and the rest rather than allocated disproportionately to the rich.

In the post-World War II period from 1945 to 1980 the growth in national income (not the total national income) on average was shared 35% to the top 10% of income earners and 65% to the remaining 90%. About 30% of the workforce was unionized, and many workers had received extensive on-the-job training in wartime factories. College tuition at state universities was heavily subsidized by the states. The middle class comprised well over 60% of the population. The income tax rate topped out at 91% until the Johnson administration, following Kennedy’s initiative, lowered it to 75%. The economy thrived with only modest periodic recessions buoyed by strong pent-up demand from savings built up during the war through the purchase of war bonds. The federal government balanced its budget while building the federal highway system.

All that changed, beginning with the neoliberal Reagan administration in 1981 dedicated to the enrichment of the wealthy and the immiseration of the rest. By cutting the top marginal tax rate from 70% to 28% and raising payroll taxes, Reaganomics shifted the tax burden toward the middle class. Deregulation and bloated military spending further redistributed income upward so that by the end of the Reagan administration, the share of the growth in national income garnered by the top 10% of income earners rose to 87%, leaving only 13% to be distributed to the rest. (The ratio increased to 98% to 2% during the reprise of Reaganomics under the G.W. Bush administration! Reagan also began de-unionization by breaking the PATCO strike so that today, only about 7% of the workforce is unionized. The middle class shrunk to well under 50% of the population. Reagan also initiated the defunding of state universities as Governor of California, a trend subsequently carried on by neoliberal federal and state governments, resulting in today’s massive student debt load. (For an excellent account of this upward redistribution of wealth, read Thom Hartman’s The Hidden History of Neoliberalism: How Reaganism Gutted America and How To Restore Its Greatness) In short, because of the continuation of neoliberal policies, the U.S. now exhibits the greatest inequality among advanced nations.

The working classes would enjoy a rising standard of living supported by rising real wages, thereby reducing their need to borrow to sustainable levels and providing a chance to save for a change.

Workers would no longer be trapped in a spiral of ever-increasing debt and could enjoy the security of savings for contingencies and retirement.

A reconstituted, secure middle class would engender political tranquility. Thus, it would serve the long-term interests of wealthy corporate managers and owners.

The rich would still enjoy substantial gains in income and wealth but with less money to spend on extravagances and smaller surpluses to invest.

As the need for workers to borrow diminished, so too would the allocation of the surpluses of the rich as debt to the working classes, increasing the proportion of said surpluses allocated to productive capital investment to the benefit of all.

Growth of the economy would no longer be based on unsustainable increases in the burden of debt imposed on the working classes, thereby reducing inequality and eliminating, or at least attenuating, one of the primary sources of significant economic contractions and financial trauma.

The graph above shows the complete picture of how the wealthy invest their surpluses now: What is not loaned to households flows a) into businesses either as direct loans from banks or into the stock and bond markets through the intermediation of investment banks, which are either independent or affiliates of commercial banks (inadvisedly ever since the 1999 repeal of the 1933 Glass-Steagall Act), and b) into commodities, precious metals, bonds, real estate, art, bananas (!), and in recent years, crypto tokens, etc. through the intermediation of corresponding brokers. The sheer volume of these surpluses flowing into financial and housing markets, coupled with “irrational exuberance,” eventually produces dangerous bubbles, the bursting of which triggers major economic contractions, evaporating much of the surplus that produces these calamities.

An economy dependent for growth on an ever-increasing burden of debt levied on the working classes must eventually collapse when the burden becomes intolerable both financially and politically. Democracy’s supreme virtue lies in the ability of an aggrieved population to find relief by changing rulers peacefully at the ballot box. Authoritarian systems, on the other hand, invariably resort to escalating repression when the collapse occurs, resulting in revolutionary violence in the population’s quest for relief.

Regrettably, the dominant cabal within the oligarchy today fails to recognize the ultimately self-destructive consequences of its primordial pursuit of unlimited wealth and unbridled power at the expense of the working classes upon which its wealth depends. I suspect these worthies genuinely believe the fate of the country best rests in their grasping hands, little realizing the dangers the inequality they embrace poses to themselves, their enterprises, the country, and indeed, the world. Notably, Czar Nicholas, King Louis XVI, Adolf Hitler, and Benito Mussolini suffered from the same myopia.

As I argue in the segment immediately above, a more equitable distribution of productivity gains would eliminate, or at least attenuate, economic and financial trauma; promote a prospering, secure, contented middle class; and engender political tranquility. Thus, more equitable sharing would serve the long-term interests of wealthy corporate managers and owners who depend on the middle class as customers. After all, Henry Ford, despite his faults, recognized that paying his workers well would provide them with the wherewithal to buy his cars.

Thankfully, there has always existed within the ranks of the moneyed class a substantial fellowship that recognizes both the dangers of extreme inequality and the necessity of achieving a more equitable distribution of the fruits of prosperity. They are conscience-driven, wealthy philanthropists like Andrew Carnegie, once the richest man in the world, who also, despite faults, funded 2,800 libraries around the world to promote education. “Saying that, ‘the man who dies rich dies disgraced,’ he reinvented himself as a philanthropist and spent his later years using his fortune for the betterment of society. Carnegie funded retirement pensions for teachers, established the Carnegie Institute of Technology (later Carnegie-Mellon University), and set up scientific research centers and organizations devoted to world peace. He also furnished towns across the globe with everything from music halls and swimming pools to church organs.” (Source: history.com.) Cornelius Vanderbilt, having amassed the largest private fortune in the U.S. at the time of his death in 1877, left an enduring legacy of philanthropy, including Vanderbilt University and generous support of churches, hospitals, and charitable organizations. Today Warren Buffett, Bill and Melinda Gates, and many other extremely wealthy individuals join the ranks of previous members of the fellowship of philanthropists. Whether with the wisdom of age and a break in the primordial fever of wealth accumulation, Elon Musk, Jeff Bezos, Mark Zuckerberg, Larry Page, Sergey Brin, and others will join them and help save the world, remains to be seen. Alas, I fear a similar regeneration of our next president is a bridge too far.

TO BE CONTINUED IN PART IIIB TOMORROW.