THE UPSIDE OF THE DOWNSIDE - PART IIIB

Causes and Consequences of Income/Wealth Inequality

2024 IS THE NEW 1928

There exist disturbing financial parallels between 1928 and 2024 explaining the inevitability of another crash and great depression á la 1929 and 1930s: Then, as now, the unprecedented wealth created by the commercialization of highly profitable new technology in the “good times” of Phase I of the Megacycle flowed disproportionately upward to corporate top management, shareholders, and Wall Street financiers, aided in no small part by legislation enacted by pliant politicians beholden to their wealthy donors. This maldistribution of wealth exacerbated inequality between the rich and the rest, creating excessive debt, thereby setting the stage for the “hard times” of Phase II, as described in the previous models.

The Second Industrial Revolution (ca. 1895 to 1980)

For a description of the basic timeline of the Second Industrial Revolution, see Part II of this series. The paragraphs below flesh out the salient economic and financial events of this Megacycle.

The 1920s witnessed the introduction of a new phenomenon: formalized consumer credit systems. The mass production of consumer goods fueled an initially virtuous cycle of consumer credit extended to working-class households, funded by the extraordinary surpluses of the wealthy, who in turn profited from the credit-financed sale of goods from factories they owned and/or managed. Rinse and repeat. However, the cycle turned vicious as the growth of household debt outstripped the gains in wages, prompting households eventually to trim spending, thereby arresting and later depressing corporate sales and profits as debt-burdened consumers either stopped borrowing or defaulted in large numbers. Shrinking sales prompted layoffs, in turn producing more defaults and less spending. Less demand prompted more layoffs, and so on, in the downward spiral of the Great Depression of the 1930s.

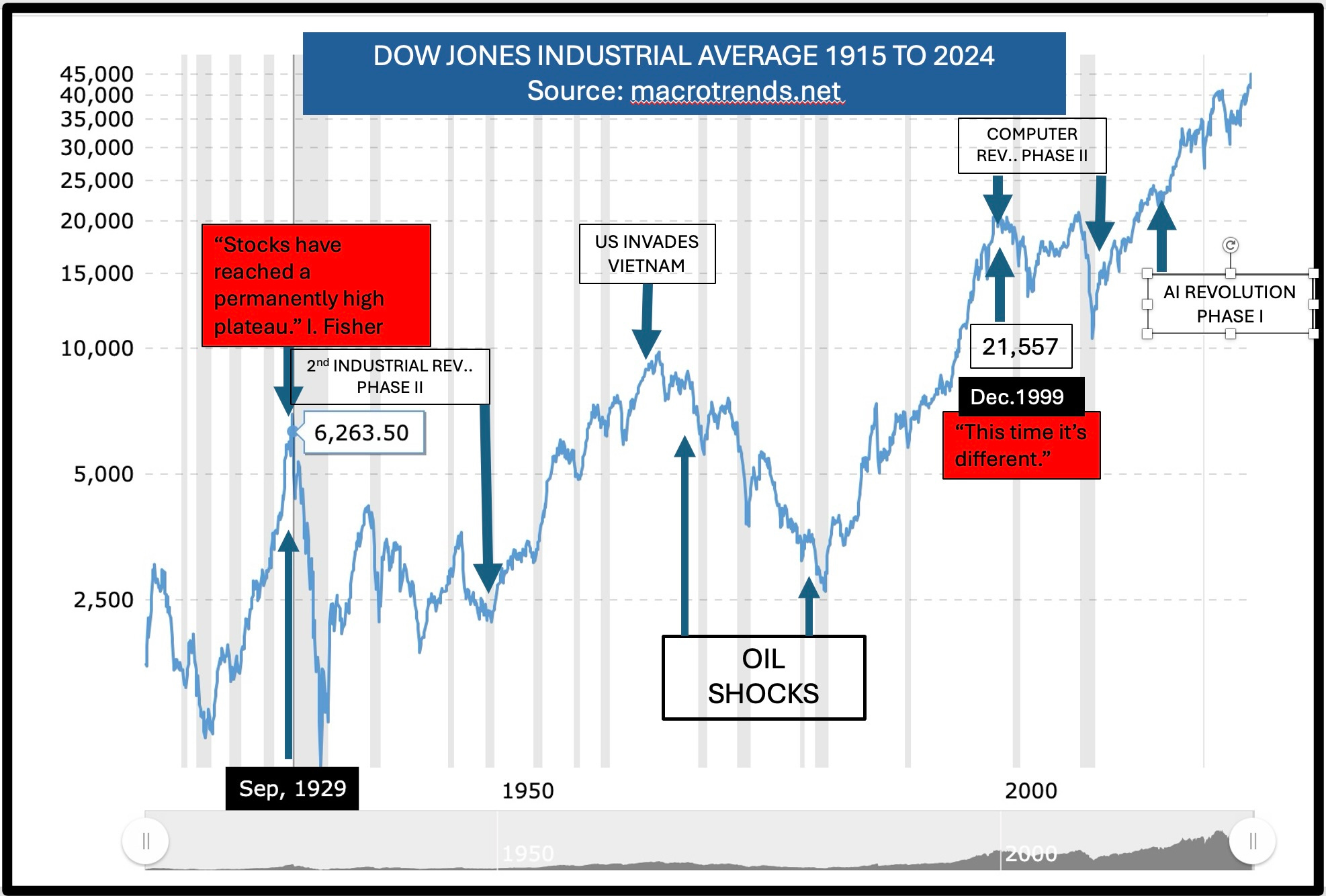

These events reverberated in the stock market. In the Roaring Twenties, stock prices soared in tandem with surging corporate sales and profits in the early virtuous stage, magnified by greed-driven investors speculating with as much as 10:1 leverage in margin accounts. Corporate sales and profits were, in turn, themselves highly leveraged by management seeking to maximize return on investment. The same applied to many undercapitalized banks. “Easy money” sparking greed in those halcyon days prompted overproduction of agricultural and industrial goods. However, in 1929, as the outlook for sales and profits darkened when consumers became overburdened by debt, the cycle turned vicious; managers and speculators quickly learned that leverage cuts both ways, exacerbating the decline in profits, in turn steepening the decline in highly leveraged stock prices, creating panic and plunging stock prices beginning in October 1929. The Crash marked the beginning of Phase II of the Second Industrial Revolution, the 3-year bear market, and Great Depression of the 1930s. The overriding flaw in the system precipitating the collapse of the stock market and economy was TOO MUCH DEBT as a consequence of income/wealth inequality.

The recovery began in 1933 as the incoming Roosevelt administration “primed the pump,” restimulating demand by providing jobs in the Civilian Conservation Corps, the Tennessee Valley Authority, the Works Progress Administration, and many other reforms you can learn about by clicking here.

In simplest terms, Roosevelt succeeded where Hoover failed because, beyond building the Hoover Dam, Hoover essentially did nothing, remaining stuck in Alfred Marshall’s classical economic theory based on the flawed notion that free markets would self-correct through wage decreases in response to changes in the supply and demand for labor (i.e., high unemployment would lower wages to the point where business would put the unemployed back to work, reversing the downward spiral.) However, both Hoover and Marshall underestimated the “stickiness of wages” and the demoralization of fearful business executives and owners, unwilling to ramp up production in the face of weak demand, and likewise, the reluctance of fearful bankers to lend in the face of rampant defaults. Roosevelt, on the other hand (who famously said, “The only thing we have to fear is . . . fear itself.”) adopted John Maynard Keynes’ theory, figuring if business and banking were frozen into inaction by fear, the government must step in and put the unemployed to work on government projects to revive demand, in turn giving business the incentive to hire the unemployed and ramp up production, thereby reversing the downward spiral.

The 1930s Great Depression ended conclusively, and Phase III, sustained, mature growth, began around 1940, with the government’s mobilization of industry undergirding the military build-up to fight World War II (Keynes’ theory on steroids). The stock market reflected the shift to Phase III beginning in June 1942 when victory in the Battle of Midway reassured prescient early investors of the ultimate favorable outcome of World War II. The ensuing bull market persisted after the war, sustained by mature U.S. economic growth to meet the pent-up U.S. demand for consumer goods and housing, the postwar rebuilding of Europe and Japan, and the building of Eisenhower’s Interstate Highway System. The postwar bull market ended in 1966, shortly after the U.S. invaded Vietnam in March of 1965. (See graph of 100 years of the Dow Jones Industrial Index below.)

Beginning with the Arab/Israeli War and the Oil Embargo in 1973, oil shocks finally upended Phase III of the Second Industrial Revolution, producing rampant inflation, high interest rates, two recessions, and the worst stock market of the postwar period. The eventual collapse in oil prices in 1986 occurred as a consequence of a sustained campaign by central banks around the world (led by the U.S. Federal Reserve Bank) to curb the demand for oil by restraining the U.S. and global economy with high interest rates (“tight money”). The combination of flat demand for and expanding deliverable supply of oil in response to high oil prices led inexorably to an oversupply of oil, causing oil prices to collapse. Beginning in late 1985, oil prices (officially $34/barrel and as high as $40 on the spot market) plunged to $10/bbl by March 1986. Low oil prices in the latter half of the 1980s then spurred the bull market in stocks associated with Phase I of the Computer Revolution.

The Oil Shocks episode ultimately relates to Megacycles insofar as:

Oil shocks presage the inevitable, eventual shift in dominant energy source, much like the shift to coal in the First Industrial Revolution and to oil in the Second. I say “inevitable shift” inasmuch as oil as a finite, diminishing resource must eventually be replaced by alternative energy sources, including renewables and, hopefully, hydrogen fusion and geological hydrogen.

Changes in oil prices dominated financial and economic cycles for decades after the first oil shock in 1973. I built a 24-year career of accurate forecasting based on this principle. My first paragraph as a newsletter writer on July 4, 1984, began: “The economic outcome over the foreseeable future will be determined, as it has been during the past decade, by the contest between the interests of oil and industrial capital over the price and availability of oil.”

The Computer Revolution (ca. 1980- ca. 2015)

The end of the Second Industrial Revolution and the beginning of the Computer Revolution arguably occurred around 1980, with the introduction of the personal computer and related innovations driven by electronic technology (which originated with Bell Labs's invention of the transistor in 1947). See Part II of this series for the timeline of this revolution. The paragraphs below flesh out the salient economic and financial events of this Megacycle.

The Dot.com Bust in 2000-2003, The Crash of 2008, and the Great Recession of 2007-2009

In 2000 and 2008 we witnessed what can be described as a repeat of the 1930s and a preview of coming attractions when the same credit-fueled, greed-driven mechanism pumped up dangerous bubbles in the stock and housing markets.

The bursting of these bubbles resulted in two bear markets and recessions when a) the Dot-Com bubble burst in 2000-2003 with a Darwinian shakeout of weaker players and b) the housing collapse, Panic of September 2008, Stock Market Crash of 2008 and Great Recession beginning in the 4th quarter of 2007 and ending in the first quarter of 2009. (See: Wealth Inequality Caused the Great Recession.)

The very existence of extreme inequality of income and wealth provides a red flag warning of an impending catastrophe.

What have we learned from this analysis of the Megacycles of the Second Industrial Revolution and Computer Revolution?

The continued growth of the economy where the rich gather up all the marbles depends on a constant, unsustainable increase in household debt, becoming intolerable as the growing burden of debt service eats into budgets limited by stagnant wages. Household spending cuts and defaults follow, housing prices collapse, credit dries up, the economy slumps, as do corporate sales and profits, stock prices plunge. Companies then lay off workers, and a vicious cycle ensues as businesses faced with slumping demand for their products lay off yet more workers, further reducing demand and undermining capital investment in new plant and equipment, causing yet more layoffs and defaults. Rinse and repeat.

A similar downward spiral can occur if the stock market crashes due to a sudden shift in investor sentiment, sparked by shrinking profits either from diminished demand, described in the previous paragraph, or from diminishing returns from over-investment in the new technology, like the Dot-Com bust in 2000-2003. With sophisticated insight into the coming shakeout, savvy Big Money investors usually initiate the shift in investor sentiment, deciding it’s time to pull out of the market, leaving small investors holding the bag, and then scooping up stocks of the survivors at bargain prices when the market bottoms and rebounds. Bernard Baruch famously decided it was time to cash out before the 1929 Crash when he got a stock tip from his shoeshine boy.

It’s the recurring nightmare of unbridled capitalism. Not fatal, as it turns out, and, as Schumpeter points out, “creative destruction” is ultimately salutary as weak enterprises are weeded out, and surviving companies emerge stronger when the economy recovers. But there’s a steep cost to be paid.

The Artificial Intelligence Revolution (ca. 2015 - ????)

The situation today: Well, guess what? The present neoliberal plutocracy remains dominated by Reaganomics despite President Biden’s best efforts to override it. Legislated inequality initiated by the Reagan administration inducing the maldistribution of profits from productivity gains spurred by new technology remains with us today in spades, and so is the rampant greed of the oligarchs, irrational exuberance in the stock market reflected in unusually high stock valuations associated with the rush to invest in new technology, unaffordable housing prices and rents, and a near-record ratio of total U.S. debt (household, corporate, and government) to gross domestic product – all signs echoing conditions in 1928 pointing to an approaching stock market crash and severe economic contraction.

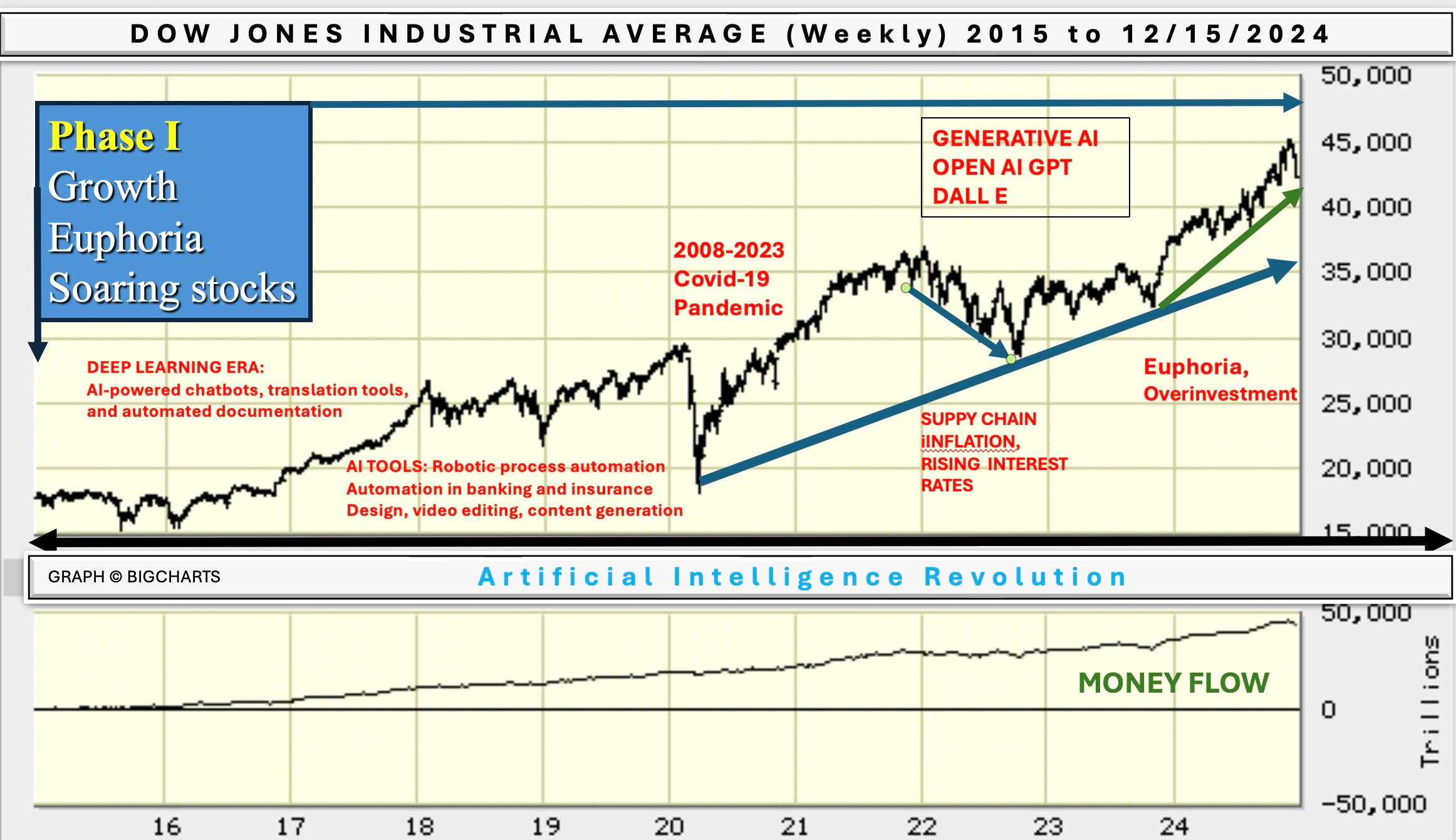

The AI Revolution Phase I: Soaring Stock Market 2016 to December 15, 2024

The graph above shows the Dow Jones Industrial Index response to the progress of the first phase of the Artificial Intelligence Revolution beginning around 2015:

The Phase I bull market begins in 2016 with the Deep Learning Era as productivity soars with transformative applications such as AI-powered chatbots, translation tools, and automated documentation. Additional productivity gains stem from automation at scale with AI tools like robotic process automation in factories and automating repetitive tasks in banking and insurance, tools for design, video editing, and content generation in creative industries.

The bull market suffers a setback in 2020 caused by the Coronavirus/COVID pandemic (an exogenous variable, like the Oil Shocks of the 1970s, referred to in Wall Street as a “black swan” event), producing an immediate panic, stock market crash and recession in 2020-early 2021 followed by a recovery.

In 2022, stocks swoon again due to worldwide inflationary COVID supply-chain disruptions driving up interest rates, slowing the economy, and cooling the overheated housing market.

The stock market then recovers in late 2022 following the introduction of Generative AI (Open AI’s GPT series and DALL E), shifting into high gear in late 2023 as money floods into AI-related companies, propelling stocks skyward into the euphoric, “irrational exuberance” stage similar to that of 1928 and the Dot-Com boom in the late 1990s. And that’s where things stand today. You will know the end of the bull market is near when the cry goes up on Wall Street: “This time it’s different.” (You heard it in October 1929 when Yale economist Prof. Irving Fisher famously declared, “Stocks have reached a permanently high plateau,” and in 1999 at the height of the Dot-Com bubble.)

As is typical with the introduction of all new technology, over-investment in AI will eventually produce winners and losers (remember the Blackberry?), causing a shakeout and plunging stock market, as it did in 1929 following the boom in the manufacture of electromechanical products like cars, appliances, and radios and again in 2000 when the Dot Com bubble burst.

Phase I: TOO MUCH DEBT

As previously argued in these pages, the existence of TOO MUCH DEBT, as a result of inequality in the distribution of income and wealth, inevitably causes major economic contractions.

As of June 2024, the ratio of total U.S. debt to Gross Domestic Product at 730% is hovering near record highs (except for the Covid-related surge in the early 2020s), roughly the same as the level in 2008 precipitating the G.W. Bush-era stock-market crash, banking crisis and Great Recession. (N.B. The beginning of the sharp climb of this ratio coincides with the introduction of Reagan’s economic policies in the early 1980s serving his rich donor class: tax cuts mainly for the wealthy, deregulation, de-unionization, and bloated military spending. Since wealthy individuals own most debt instruments (e.g. bonds, bank deposits), the rise in the ratio reflects their soaring fortunes thanks to The Gipper, producing today’s extreme levels of financial inequality.) Forewarned is forearmed. Remember what I stated earlier: “The overriding flaw in the system precipitating the collapse of the stock market and economy was TOO MUCH DEBT” as a consequence of income/wealth inequality.”

BOTTOM LINE:

If past is prologue, as I have argued, the U.S. and world stock markets and economies will undergo another crash and major contraction, plunging the AI Revolution into the economic, financial, and political turmoil of Phase II of the current Megacycle. The warning signs of this impending calamity include:

Gross inequality in the distribution of income and wealth

A dangerously high level of total debt

Skyrocketing stock prices reaching dangerous levels of overvaluation, coupled with euphoria and low levels of fear on Wall Street

High prices and rents for housing

Potentially destabilizing fiscal and monetary policy changes to be discussed in the next installment

The dominoes are set to fall. The next question, therefore, is not if but when.

Anyone who claims to know for certain when the stock market will turn down, or the economy will contract either doesn’t know what they’re talking about or doesn’t know that they don’t know. The first rule of forecasting is (tongue in cheek) “If you give a price, don’t give a date.” If you must give a price and a date, then the second rule is . . . “forecast often.”

Since this exegesis is already long, sorely trying your patience and attention span, I’ll defer until the next part of this series consideration of the timing of these events, which is heavily dependent on the reactionary policies of the incoming administration. This will segue nicely into an analysis of the political consequences of the predicted economic and financial turmoil. From there, we will move into more pleasant subject matter: how we will get out of this mess and what constructive policies would, if implemented, repudiate the oligarchy, rebuild the middle class, restore democracy, reform and rebalance the government, and reconstruct the economy to meet the necessities of the new technological era. Stay tuned.

END NOTE

A return to the more equitable income/wealth distribution pattern of the post-World War II period is clearly desirable for the Life, Liberty and pursuit of Happiness of We the People, by and for whom the republic was founded. Ironically, it is the end result desired both by liberal Democrats and MAGA Republicans. Their disagreement is over how to achieve it (to be addressed in subsequent parts of this series).

There exists within the ranks of the moneyed class a substantial philanthropic fellowship recognizing the dangers of extreme inequality and the necessity of achieving a more equitable distribution of the fruits of prosperity. (See Part IIIA) However, they are presently outnumbered and outspent by a cabal of oligarchs hellbent on running up a big score in wealth and power by blocking more egalitarian policies with a stranglehold on government through the Republican party. Ironically, in its overzealous primordial quest for limitless wealth and unrestrained power, the oligarchy has created the very economic and financial configuration for another Great Depression, undermining their wealth and ultimately producing the revolutionary change in political will to depose them and right the foundering ship of state. Sadly, given the agitated state of American politics these days, there seems little prospect of the oligarchy recognizing the self-defeating consequences of their quest and joining their philanthropic brethren in their support for a rising tide that lifts all boats.

It’s a recurring pattern of behavior as old as the institution of government itself. Whether the people will exercise their right to alter or abolish a Form of Government destructive to Life, Liberty and the pursuit of Happiness peacefully at the ballot box or with pitchforks remains to be seen, as does the prospect of civil or foreign war instigated by the oligarchy and their minions in Washington seeking to preserve their wealth and power under the pretext of unifying the country.

Will we remember the past or be condemned to repeat it?

I’m grateful for the surge of new subscribers in response to Parts I and II of this series. I hope you recognize the importance of what is written on these pages, and, if you think well of the idea, follow Mike Monett’s recommendation:

REFERENCE:

REAGAN’S LEGACY: “It Ain’t Just a Question of Misunderstood,”

"A return to the more equitable income/wealth distribution pattern of the post-World War II period is clearly desirable for the Life, Liberty and pursuit of Happiness of We the People, by and for whom the republic was founded. Ironically, it is the end result desired both by liberal Democrats and MAGA Republicans. "

Please tell me how "We the people" is an aspect of the end result desired by both liberal Democrats and MAGA Republicans. From my experience of living within the present American nightmare, the MAGA Republicans have a very different idea of what constitutes "WE THE PEOPLE" THAN liberal democrats do. That difference is the very root of racist America, is it not?