THE STOCK MARKET IS STILL CRASHING- PART 2

Trump's Tariff Shock Heightens Fears of Inflation, Recession,and Further Stock Losses Fed, US Dollar, and Gold Markets React To President Trump's Tariff Executive Orders Best viewed in email/online.

MONETARY POLICY/THE FED: Yahoo Finance reported on April 11: “The Fed would ‘absolutely be prepared’ to deploy its various tools to help stabilize the financial markets if the need arose, Boston Fed President Susan Collins told the Financial Times in an interview published Friday. . . The higher the tariffs are, the more the potential slowdown in growth as well as elevation and inflation that one would expect," Collins said in a separate interview with Yahoo Finance earlier Friday, adding that she expects inflation to rise "well above" three percent this year, but no "significant" economic downturn. . . Growth 'below one percent'”

This statement supporting stock prices, while not unusual,[1] puts the Fed in an awkward position. Presumably, to “stabilize financial markets,” the Fed would “print money” to be injected into the banking system by buying Treasury bonds (“Treasurys”), the immediate effect being to raise bond prices and make more cash available to buy stocks, potentially boosting stock prices as well. The added cash in the banking system, plus lower interest rates prompted by higher bond prices, would support economic growth while simultaneously adding to the inflationary pressures generated by Trump’s trade war. (“Too much money chasing too few goods” produces inflation.) Accordingly, the Fed’s financial market stabilization would put the objectives of its “dual mandate” of full employment and price stability in conflict with each other – a not unusual situation.

The Fed’s ultimate decision on which policy to enact typically depends on the outcome it perceives as the greater threat. During the Oil Shock era in the 1970s and early 1980s, then-Fed Chairmen Arthur Burns and Paul Volcker prioritized price stability, sacrificing full employment by inducing massive recessions to reduce oil demand in a successful effort to lower oil prices. Their successors, Alan Greenspan (1987-2006), Ben Bernanke (2006-2014), and Janet Yellen (2014-2018), focused on full employment through “easy money” policies aimed at preventing or ameliorating recessions. They enjoyed this flexibility as they faced a diminished threat of inflation from high oil prices, given that the U.S. economy became increasingly service-oriented, reducing oil dependency as a primary driver by half.

Jerome Powell (2018-Present) will be facing the worst of possible worlds, given the confluence of forces simultaneously driving the U.S. and world economies into another Great Depression and an alarming surge of inflation.

Forces driving economic contraction:

The complex forces of Megacycle Phase II described in THE UPSIDE OF THE DOWNSIDE series Parts I through IIIC include the upward redistribution of wealth generated by new technology at the expense of the working classes (heightened by politically motivated tax cuts for the wealthy); the corresponding overinvestment in stocks by the wealthy, which sets the stage for a stock market crash; and unsustainable increases in working-class consumer and mortgage debt to compensate for stagnant real wages, ultimately resulting in cascading defaults and economic and financial collapse. (N.B. The same combination of these forces produced the Great Depression during Phase II of the Second Industrial Revolution in the 1930s, the Dot-Com bust, and the Great Recession during Phase II of the Computer Revolution in the first decade of the 21st century, and I predict will cause another stock market crash and Great Depression in this century’s second decade during the second phase of the AI Revolution, which began on March 11, 2025.) (See THE STOCK MARKET IS CRASHING.)

The negative impact on world trade resulting from Trump-ordered tariff increases. (NB: higher tariffs create stagflation, simultaneously hindering the growth of world trade and increasing inflation due to the elevated prices consumers pay for tariffed goods and the decreased supply of goods and services caused by trade barriers.)

The added dampening of aggregate demand for consumption and business capital investment caused by higher interest rates responding to the inflation created by Trump’s tariffs.

Further upward pressure on interest rates caused by the Treasury’s issuance of new bonds to finance the Republican-legislated deficits produced by tax cuts for the wealthy donor class.

(Potentially) Higher interest rates caused by the Fed attempting to dampen inflation. (See below.)

Forces driving a surge in inflation:

Higher domestic prices of foreign goods and services caused by the reduction in supplies caused by the trade war and the weakening dollar, as well the added cost of tariffs imposed on imported goods and services paid by U.S. consumers.

Higher natural gas and associated electricity prices caused by skyrocketing demand for electricity by data centers created to meet the surging requirements of the AI Revolution and the global shift toward electrically powered transportation.

Higher wage costs caused by Trump’s mass deportation policies, reducing the supply of labor.

(Potentially) Inflation caused by new money injected by the Fed into the private sector to “stabilize financial markets.”

Which policy will Powell’s Fed adopt? Much like Schrödinger's cat, we won’t know the outcome until we open the box.

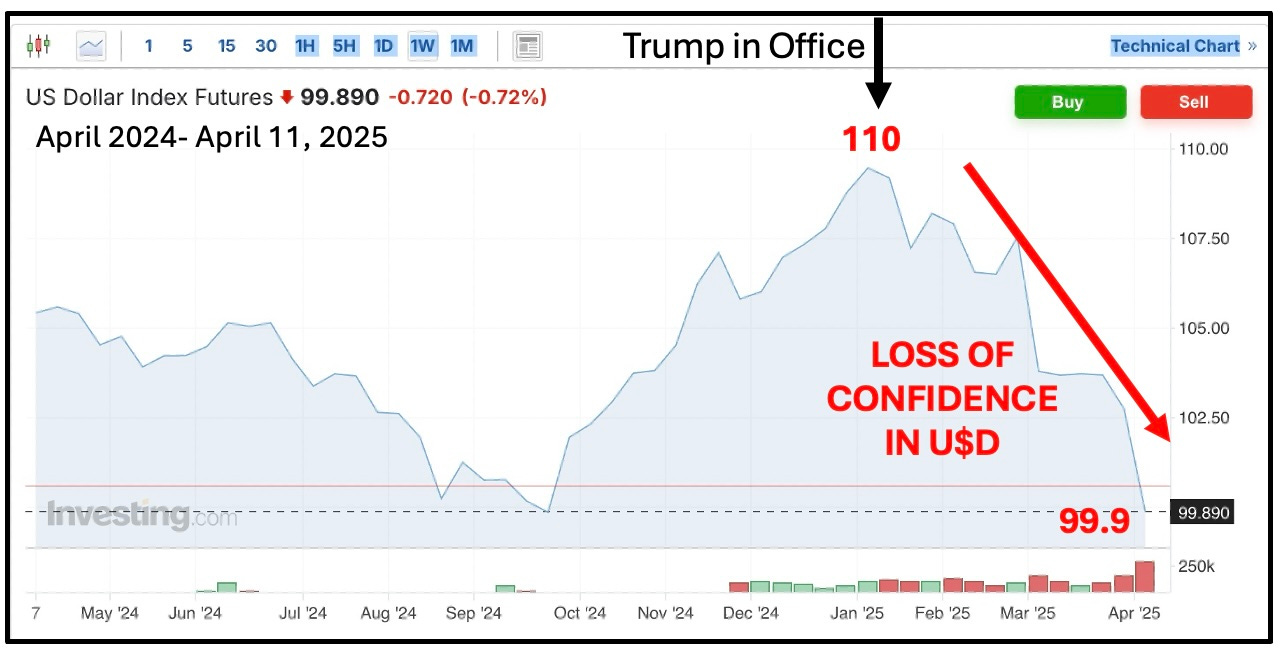

U.S. DOLLAR: For about the last 15 years, the U.S. Dollar Index has been trending unevenly higher, climbing from lows around 73 in 2010 to a sideways trading range between 100 and 110 over the past 3 years. The latest fluctuation within that range began last October at around 100, increasing to just under 110 in early January 2025 before starting a decline to 103.9 just before Trump’s April 2 tariff announcement. In the nine days following the announcement, the dollar index abruptly dropped further by 4.6% to 99.9 on April 11 at the lower extreme of the trading range - a decline that significantly reaffirmed the loss of confidence in the dollar that has persisted since Trump took office last January.

GOLD: A bull market in gold began in earnest in 2019 as prices surged from a previous plateau of around $1,250/oz to more than $3,000 during the next six years. As a global market, gold prices tend to reflect events with worldwide repercussions. Accordingly, factors prompting higher gold prices include:

Flight to safety amid global uncertainties such as U.S.-China trade tensions, the Covid-19 pandemic, the Russian invasion of Ukraine, and conflicts in the Middle East, including Gaza, Yemen, and Syria. Disruptions in trade and supply chains, along with interruptions in oil supply from oil-producing regions, have inflationary implications, leading investors to purchase gold, the traditional hedge against inflation.

Low interest rates diminish the opportunity cost of holding gold, which pays no interest or dividends. Central banks worldwide pushed interest rates to near-zero between 2020 and 2022 through quantitative easing (“printing” money), to sustain their pandemic-stricken economies, with the influx of new money heightening inflationary concerns. (Conversely, higher interest rates usually suppress gold prices by increasing the opportunity cost of holding it.)

The value of the dollar typically relates inversely to the price of gold. Since gold is priced in dollars worldwide, a weak dollar requires more dollars to purchase an ounce, meaning higher gold prices expressed in dollar terms. (Conversely, a strong dollar generally means a dollar can buy more gold, effectively resulting in a reduction in gold’s price.)

Gold purchases for jewelry, particularly in China and India, push up gold prices.

Purchases or sales by central banks and investment funds, not necessarily tied to specific economic outcomes can influence the price of gold unpredictably.

Recently, gold appears to be caught between conflicting signals. Following Trump’s Liberation Day announcement on April 2, gold prices mirrored the stock market, declining by approximately 5.6% from a peak of around $3,150 per ounce to $2,975 on April 7. This drop was likely due to expectations of a trade-war recession, typically accompanied by abating inflation and lower interest rates, which tend to depress gold prices. However, immediately after Trump’s tariff pause announcement on April 9, gold investors reassessed the situation, driving the price of gold up to $3,237 by the close on April 11, probably because of:

Fears of rekindled inflation stem from both domestic price increases linked to tariff pass-throughs and shortages caused by interruptions in the supply of essential goods from China, many of which the U.S. no longer produces.

The weakening dollar reflects a loss of confidence in the currency among U.S. trading partners, buffeted by Trump’s aggressive and erratic trade policies.

While the increase in U.S. bond yields would tend to depress gold prices, gold investors may be looking beyond the higher opportunity cost of rising rates to the inflationary rationale behind the rise.

SUMMARY: In my 24 years publishing my Cyclical Investing newsletter (1984-2008) and speaking on the national/international stage, rarely have the benchmark financial market indicators – stocks, bonds, oil, currency, gold -- unanimously pointed to the same outcome as they now do. In the present instance, they point to resurgent inflation and rising economic entropy for sure – with either a) slow-to-no growth (i.e. stagflation) or b) an economy contracting somewhere between recession and another great depression. The Fed, agrees on inflation but, always reluctant to call a recession lest it cause one, goes with the milder, more palatable alternative of slow growth. Being a contrarian deep into thoughts of Phase II of the AI Megacyle, I’m sticking with my prediction of a stock market crash and great depression.

NOTE TO SUBSCRIBERS: As you have no doubt noticed, I don’t flood you with daily posts, nor do I pester you to upgrade to a paid subscription. There are reasons for this. When I send out a post, I want it to stand out as newsworthy and important for you to read,. Regrettably, only about half of you do so, according to Substack analytics. I hope over time, the rest of you will realize the value of what’s being communicated in this space and read every post. My objective is “to provide the most valuable information you can use and the most expensive advice to ignore.” (If you see that epigram elsewhere, know I originated it.)

I have no paid subscribers, nor do I intend to solicit paid subscriptions, ever. I’m not in this to make money and have no need to do so. What I share with all committed writers is the conviction, proven over the course of a successful 40-year career as a newsletter writer, public speaker, and now Substack blogger, regarding the value of my thoughts, along with a writer’s innate impulse to replicate them in the minds of as many readers as I can reach.

So, if you share a committed reader’s innate impulse to reciprocate when receiving a gift, assist me in extending that reach by recommending the Cassandra Chronicles to people you care about.

Please leave a comment to let me know you are there.

[1] Famously, a similar one-line statement by Fed Chairman Alan Greenspan in response to the October 19, 1987 “Black Monday” stock market crash singlehandedly turned the market around, allaying fears of a reprise of the Great Depression: "The Federal Reserve, consistent with its responsibilities as the Nation's central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system"