THE STOCK MARKET IS STILL CRASHING

Trump's Tariff Shock Heightens Fears of Inflation, Recession and Further Stock Losses Part 1: Market Reaction: U.S. Stocks, U.S. Bonds, West Texas Intermediate Crude Oil. Best viewed in e-mail/online.

A lot has transpired during the first 80 days of the second Trump administration, none of it beneficial, covered admirably and in detail by other Substack authors I refer you to in the following footnote. 1 I will refrain from duplicating their efforts in describing the administration’s “deconstruction” (or, more accurately, demolition) of this nation’s scientific research, health care, drug development, civil rights, election integrity, academic freedom, judicial independence, civil service, consumer finances, international trade, veterans’ care, Social Security, governmental accountability, Medicare/Medicaid, worker safety, environmental protection, aviation safety, weather forecasting, cyber security, efforts to combat climate change, and more. Instead, I will outline in the broadest terms the “cascade” of financial events I warned you about beginning last December in my series THE UPSIDE OF THE DOWNSIDE, leading to the “financial/economic crash” I predicted due to fundamental, long-term economic/financial/political forces heightened by the “incoming administration’s reactionary policies. . .”

President Trump unveiled the centerpiece of his reactionary policies on April 2, 2025, “Liberation Day” -- a day which will live in, you know, infamy. Overriding Congress’ Article 1, Section 8 constitutional “power to lay and collect Taxes, Duties, Imposts, and Excises, and in the Commerce Clause, to “regulate international trade,” Trump signed EO 14257: Regulating Imports With a Reciprocal Tariff To Rectify Trade Practices That Contribute to Large and Persistent Annual United States Goods Trade Deficits.

To bypass the Constitution’s clear Congressional mandate, Trump clung to authority granted by Congress to a president in cases of “national emergency,” claiming that “the domestic economic policies of key trading partners” posed “an unusual and extraordinary threat to the national security of the United States.” With this assertion, along with interminable paragraphs of grievances, Trump imposed “ad valorem duties on all imports from all trading partners [starting] at 10 percent and shortly thereafter, the additional ad valorem duty shall increase for trading partners enumerated in Annex 1 at the rates set forth in Annex I to this order. These additional ad valorem duties shall apply until I determine that the underlying conditions described above are satisfied, resolved, or mitigated.”

The subsequently stated purposes of the tariffs included:

Forcing foreign trading partners to relocate factories within U.S. borders to avoid punitive tariffs, thereby creating U.S. factory jobs lost to “globalization,” while pointedly overlooking U.S. export jobs lost when trading partners reciprocate with increased tariffs of their own, to which we must add loss of U.S. jobs associated with the distribution of imported products.

Forcing foreign government leaders to “kiss [Trump’s] ass” (his words) to negotiate terms that would eliminate present deficits in the U.S. balance of payments with their countries.

Raising government revenues (erroneously said to be paid by foreign exporters) to help finance income tax cuts sought by Republicans, mainly to appease their donors and keep their campaign contributions coming. In effect a national sales tax, tariffs raise the cost of living, the burden falling disproportionately on the working classes, who spend virtually all they earn, whereas the wealthy spend only a fraction of what they earn, saving the rest.

An unstated objective, alleged by Democratic Connecticut Senator Christopher Murphy, was to enable certain individuals favored by Trump to profit from insider stock trading with advance notice of market-moving tariff policy changes. Trump bragged in the Oval Office about the outlandish profits his favored oligarchs made buying stocks just before the April 9th announcement of the tariff pause. According to The Hill, “House Minority Leader Hakeem Jeffries (D-N.Y.) said Thursday [April 10] that House Democrats will soon launch investigations into potential wrongdoing following President Trump’s surprising decision a day earlier to pause his reciprocal tariffs — a move that immediately caused stocks to soar.”

The widespread view in the mainstream press suggests that, shaken by the panicked responses of stock and bond investors to his tariff plans, numerous institutional forecasts of an impending recession, and an outcry from his wealthy donors, Trump relented on Wednesday, April 9, announcing a 90-day pause on the imposition of tariffs (except for China) exceeding a baseline of 10% on all imports. However, Trump and his so-called propaganda ministry at Fox News claimed that the pause was “part of the plan” to compel trading partners to negotiate terms more favorable to the U.S. We’ll see.

Financial markets were unusually clear in their assessment of the situation, uniformly expressing expectations of renewed inflation and subdued economic growth – in a word, “stagflation,” with varying opinions on the extent to which economic growth would be affected. Even the Fed concurred.

The two presidents, Xi and Trump, appear to be taking the trade war personally. On Thursday, April 10, the day after Trump announced the pause, Xi dampened the market euphoria that had followed Trump’s announcement of the 90-day pause, by declaring China’s imposition of a countervailing tariff of 125% on all imports from the U.S., effectively closing the door on U.S. trade with China.

U.S. STOCKS: In my March 12, 2025 post titled “THE STOCK MARKET IS CRASHING, " I revealed the technical breakdown of the Dow Jones Industrial Average (DJIA, Dow) benchmark stock market index, signaling the onset of the Megacycle Phase II crash I have been predicting since December 7 of last year. Closing at 41,433.48 on March 11, breaking below the triple-confirmed support level of around 42,000, the Dow signaled a technical breakdown, pulling the trigger to sell stocks. The Index rebounded briefly during the next 3 weeks, but on April 2, as news spread of Trump’s ‘liberation day’ tariff announcement, the Dow promptly plunged nearly 11% in the next 6 days to a low of 37,606 on April 8, nearly 16% below its previous peak of 44,747 in early February. This sudden drop occurred as investors awakened to the catastrophic effects on world trade and inflation implied by the imposition of unprecedentedly high worldwide, country-specific tariffs (rather than item-specific). Next day, the decision to pause triggered one of the largest stock market rebounds in history on April 9, only to be followed by a slump the following day when the administration announced it would set its tariffs on Chinese imports at a prohibitive 145% in response to China’s steadfast counter-reaction to Trump’s tariffs.

The Dow closed on Friday, April 11 at 40,212 and the NASDAQ at 16,724, down nearly 11% and 17% %, respectively, from their all-time record peaks recorded last December of 45,014.04 and 20,173.89.

While tariffs undoubtedly account for most of the recent market volatility, we should not lose sight of the underlying long-term, secular bearish forces dominating Phase II of the current Megacycle. (See THE UPSIDE OF THE DOWNSIDE – Part IIIB). Inasmuch as the technical breakdown described in THE STOCK MARKET IS CRASHING on March 11 occurred three weeks before the tariff kerfuffle, suggesting the beginning of the Phase II bear market, I expect stocks to continue declining even if the tariff issues fade into the background. Rudimentary technical analysis reveals breakdowns in both near- and long-term support and a downtrend that remains intact. (See graph.) Moreover, the stock market abhors uncertainty. Given the uncertainties associated with Trump’s stop-and-go policies, uncertainty hangs over the market like a cloud over Joe Btfsplk. Accordingly, investors who are cyclically alert and responsive will avoid stocks.

U.S. BONDS: Bond yields, which had been steadily declining for most of the year due to reassuring news of decreasing inflation and the Fed easing monetary policy with lower short-term interest rates, suddenly skyrocketed after the announcement of tariff increases. This shift indicated investor expectations of resurgent inflation and a deterioration of investor confidence in U.S. government securities as a safe haven.

In mid-January, the benchmark 10-year Treasury bond yield peaked at around 4.8%, significantly declining to 3.9% on April 2, just before the tariff announcement. Following this announcement, the yield surged to 4.49% on April 11, primarily driven by fears of inflationary consequences arising from higher tariffs. The surge in bond yields heightened economists’ expectations of a recession due to their dampening effect on aggregate demand and capital investment associated with higher borrowing costs.

Unlike the stock market, bond yields showed no signs of relief with the news of the 90-day pause. Typically more discerning than stock investors regarding the long-term outlook, bond investors communicated a clear message reflecting fears of renewed inflation and diminished confidence in U.S. Treasurys - sentiments further confirmed by soaring gold prices and a weakening dollar.

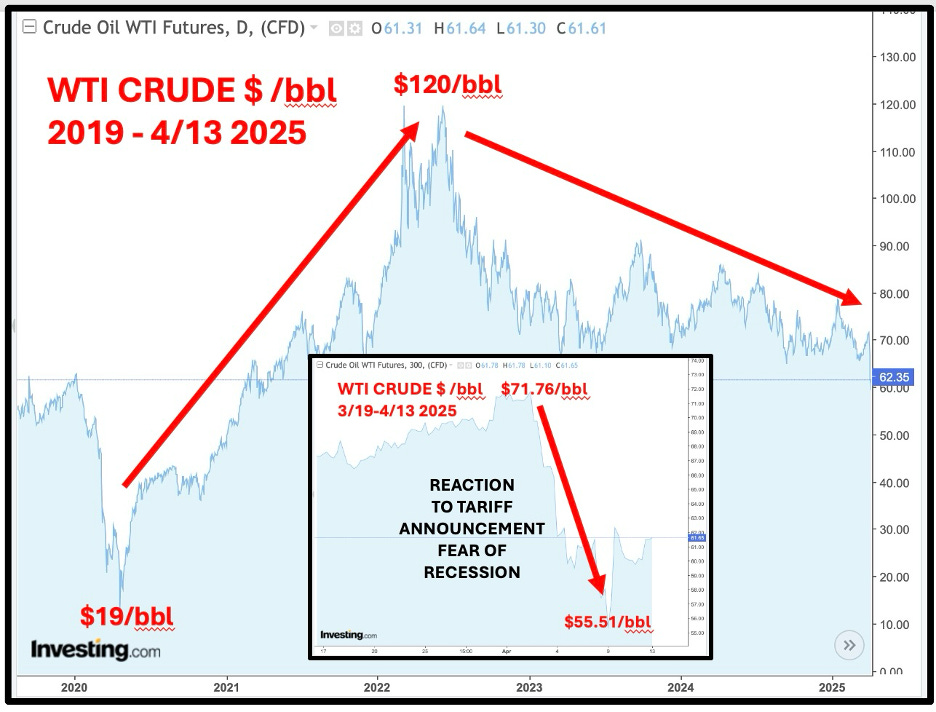

OIL: World oil prices had been trending downward for the last 3 years, since climbing from a low of $19 per barrel for West Texas Intermediate (WTI) on weak oil demand at the trough of the Covid economic shutdown in February 2020 to a peak of $120/bbl in mid-2022 on surging demand as the world economy recovered. (By the way, that spike in oil prices goes a long way to explaining the severity and duration of the inflationary surge during the Biden administration, commonly attributable only to “supply chain interruptions.”) By April 2, 2025, just before Trump’s tariff announcement, the price of WTI had eased to $71.76/bbl. Immediately after the announcement, oil plunged 23% to $55.51/barrel, reflecting the market’s expectation of a trade-war recession’s diminished oil demand. (Subsequent modest rebound to $61.336/bbl on April 13)

DUE TO LIMITATIONS ON THE SPACE ALLOWED IN E-MAILS This concludes Part 1 of the series THE STOCK MARKET IS STILL CRASHING — Trump's Tariff Shock Heightens Fears of Inflation, Recession and Further Stock Losses. Part 2 will follow shortly with the reaction of the Fed and dollar and gold market reactions to Trump’s tariff policy gyrations.

Prominent among them, Thom Hartmann, an original liberal thinker of astounding breadth, depth, and eloquence, not to mention boundless energy; Michael deAdder. Canadian cartoonist, the sharpest pen in the business; Heather Cox Richardson, who writes the first draft of history; Joyce Vance, together with her “Sisters in Law,” the quintessential translator of legalese into English we can all understand; Dan Rather, now the paternoster of journalism who has been there, done that and seen it all; Robert Reich the vox clamantis in deserto, a diminutive giant who has launched thousands of minds from his podium at U.C. Berkeley; Steve Schmidt whose daily fulminations would part the Red Sea; Michael Moore, tireless tweaker of establishment lion’s tails; Patrice Mersault, eloquent spokesperson for the opposition, Mike Brock, philosopher and wordsmith extraordinaire, and many others who exceed my limited bandwidth. . . Bless ‘em all.

💸😎

I hate that I'm cheering for Xi to be tough.